When you’re shopping for your next car, it’s tempting to boil everything down to a single number: the **monthly payment**. But with an electric car, that number is only half the story. To really compare an electric car vs a gas car monthly payment, you have to look at the *total* monthly outlay: loan or lease, fuel, maintenance, insurance, and even taxes.

Key idea

Why “monthly payment” comparisons are trickier than they look

In 2026, the **average new‑vehicle payment in the U.S. is hovering around the high‑$600s** per month, thanks to high prices and stubborn interest rates. Many buyers are stretching loans to 69–72 months just to keep that payment under control. The catch: a gas car and an electric car with the *same* monthly payment on paper can have radically different real‑world monthly cost once you factor in fuel and upkeep.

- EVs still tend to have a **higher sticker price** than comparable gas cars, especially new ones.

- Auto loan rates on EVs and gas cars are **similar by credit tier**, but incentives on EVs can lower effective APR.

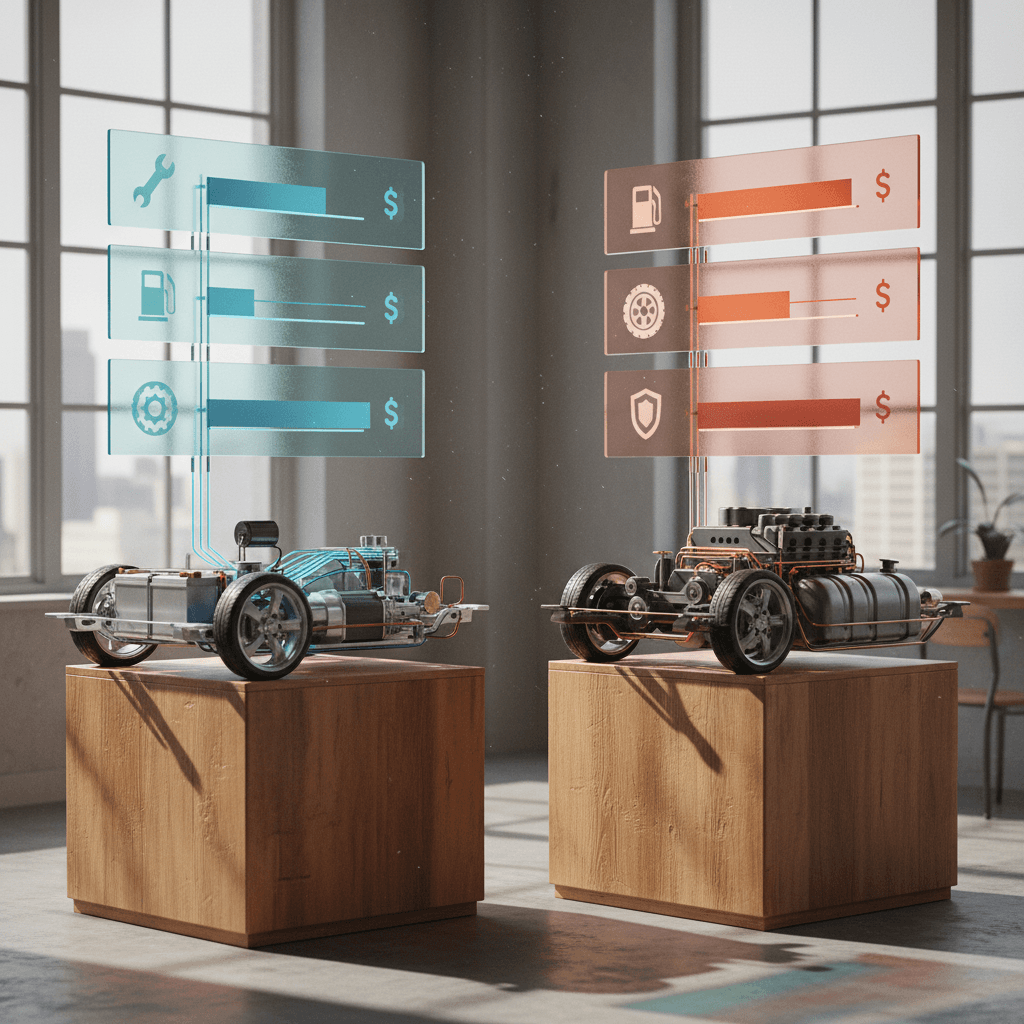

- Electricity is usually **much cheaper per mile** than gasoline, especially if you can charge at home.

- EVs generally have **lower maintenance and repair costs**, no oil changes, fewer moving parts, less brake wear.

- Insurance and tax rules for EVs have changed since late 2025, and they now matter more in the math.

Don’t compare payment alone

How to compare electric vs gas car monthly costs the right way

To get a fair **electric car vs gas car monthly payment comparison**, treat your car like a mini household budget line item. You’re not just paying for the car; you’re paying for the energy, the upkeep, and the risk.

Your real monthly cost formula

1. Start with your loan or lease payment

Note the **actual monthly payment** (or a firm quote) for each vehicle: term length, interest rate, and down payment. This is your baseline.

2. Add fuel or charging cost

Estimate your **monthly miles** (many Americans drive ~1,000–1,250 miles per month). Multiply by cost per mile: gas price and MPG for a gas car, $/kWh and efficiency (mi/kWh) for an EV.

3. Add maintenance and repairs

Roll in predictable maintenance (oil changes, tires, brakes, minor repairs). You can estimate from ownership cost studies or average bills, then divide by 12 for a monthly number.

4. Add insurance and registration

Get **actual quotes** for both cars, not guesses. Insurance can vary a lot by driver and ZIP code. Add in yearly registration/taxes, divided by 12.

5. Adjust for tax rules

In 2026, federal **loan‑interest deductions** (for qualifying U.S.-built vehicles) and the disappearance of EV purchase tax credits can shift your net after‑tax cost, especially on new vehicles.

6. Compare total monthly cost, not just payment

Add it all up for each car. The winner is the one with the **lower all‑in monthly cost**, not necessarily the lower lender payment.

Shortcut for busy shoppers

Sample scenario: new electric car vs new gas car (2026)

Let’s walk through a simplified example for a U.S. buyer in 2026 driving about **1,200 miles per month**. We’ll compare a mainstream **compact electric SUV** to a similarly sized **gas compact SUV**.

Example: new EV vs new gas SUV – all‑in monthly cost

Illustrative 2026 numbers for a typical U.S. driver. Actual offers will vary by model, state, credit, and incentives.

| Category | New EV Compact SUV | New Gas Compact SUV |

|---|---|---|

| MSRP (approx) | $50,000 | $42,000 |

| Down payment | $5,000 | $5,000 |

| Loan term & rate | 72 mo @ 6.8% | 72 mo @ 6.8% |

| Approx. monthly payment | $730 | $615 |

| Monthly fuel / charging* | $55 (home + some public) | $190 (gas at ~$4/gal) |

| Maintenance & repairs (avg) | $60 | $115 |

| Insurance (example) | $155 | $145 |

| Registration / taxes (avg) | $60 | $55 |

| Estimated tax effect** | ‑$40 | ‑$40 |

| Estimated all‑in monthly cost | ~$1,020 | ~$1,080 |

EV can carry a slightly higher sticker price and still come out ahead on total monthly cost because of fuel and maintenance savings.

In this scenario, the **EV’s payment is about $115 higher** than the gas SUV, but the EV saves roughly **$135/month on fuel and maintenance**. After insurance, taxes, and a rough interest‑deduction effect, the EV ends up **slightly cheaper overall per month** even though the sticker price is higher.

About these numbers

Sample scenario: used EV vs used gas car

The real plot twist in 2026 is on the used side. **Used EV prices have fallen faster than used gas prices**, and in many cases a used electric hatchback or crossover is now **cheaper to buy up front** than a similar gas model, while still giving you the fuel and maintenance savings.

Example: used EV vs used gas sedan – all‑in monthly cost

Illustrative 5‑year used‑car comparison for a budget‑conscious commuter.

| Category | Used EV (3‑4 years old) | Used Gas Sedan (3‑4 years old) |

|---|---|---|

| Purchase price | $26,000 | $29,000 |

| Down payment | $3,000 | $3,000 |

| Loan term & rate | 60 mo @ 10.5% | 60 mo @ 11.5% |

| Approx. monthly payment | $495 | $545 |

| Monthly fuel / charging* | $45 | $165 |

| Maintenance & repairs (avg) | $75 | $120 |

| Insurance (example) | $135 | $130 |

| Registration / taxes (avg) | $45 | $50 |

| Estimated all‑in monthly cost | ~$795 | ~$1,010 |

With used vehicles, EVs often win on both sticker price and total monthly cost.

Here, the used EV is **cheaper across the board**: lower price, lower payment, and dramatically lower fuel cost. At this point the comparison borders on unfair; the gas sedan is handing the EV owner roughly **$200–$250 per month** in savings.

Used EV catch: battery health

Financing differences: EV vs gas in 2026

The financing landscape in early 2026 is messy. **Average auto loan rates are still around 7% for new cars**, higher for used. Lenders don’t usually punish EV buyers with higher rates; they price you on credit and loan term. But a few EV‑specific quirks matter for your monthly payment comparison.

What changes, and what doesn’t, when you finance an EV

Understand how 2026 rules and incentives show up in your monthly bill.

Interest rates by vehicle type

For most buyers, **new‑car APRs** are similar for gas and EVs at a given credit tier. Used‑car APRs are higher than new for both.

Where EVs can win is via **promotional rates**, 0.0–3.9% offers that automakers quietly use to offset lost tax credits.

Loan interest deduction

The 2025 tax law created a **federal deduction for auto‑loan interest** on qualifying U.S.-assembled vehicles through 2028.

It doesn’t care if the car is gas or electric; it cares where it was built, how big it is, and how much you earn. If you qualify, your **after‑tax monthly cost** is effectively lower.

EV tax credits have changed

The big up‑front **federal EV purchase credits ended in late 2025**. That means fewer instant discounts baked into your payment on new EVs.

Automakers and dealers are filling some of that gap with **rebates and rate buys** instead, so your effective EV payment may still be lower than the sticker suggests.

How Recharged can help on financing

Fuel and charging costs per month

Fuel is where the electric vs gas monthly payment comparison usually stops being close. In 2026, national average gas prices are back around **$4 per gallon**. Electricity rates vary widely, but home charging is still almost always cheaper per mile than pumping gas, especially if you can use **off‑peak rates** or time‑of‑use plans.

Typical U.S. fuel vs charging costs (15,000 miles/year)

If you drive 1,200 miles per month, switching from a 30‑mpg gas car to a well‑chosen EV can realistically free up **$80–$150 every month** in energy costs alone. That’s real money you can redirect into a slightly higher payment, savings, or debt payoff elsewhere.

Maximize your charging advantage

Maintenance and repairs: the quiet monthly cost

Maintenance doesn’t show up as a neat line item like your car payment, but over a 5–7 year period it chews through thousands of dollars. Independent and AAA ownership‑cost studies consistently find that **EVs cost less to maintain per year** than comparable gas vehicles, even after accounting for tires and occasional service.

Why EVs tend to cost less to maintain

- No oil changes or transmission fluid service.

- Fewer moving parts in the drivetrain, no exhaust system, no timing belts, no spark plugs.

- Regenerative braking reduces brake wear; pads and rotors last longer.

- Coolant and brake fluid still need attention, but on a longer cycle.

Where gas cars hit your wallet

- Regular oil and filter changes, plus periodic tune‑ups.

- More frequent brake service in stop‑and‑go driving.

- Higher odds of **expensive repairs** past 80,000–100,000 miles, exhaust, catalytic converter, transmission.

- More systems that can trigger a check‑engine light.

Spread across a year, the gap isn’t glamorous, often **$30–$60 per month**, but paired with fuel savings it makes a noticeable dent in your real monthly cost.

Don’t ignore out‑of‑warranty risk

Insurance and taxes: what actually changes with an EV?

Insurance used to be a major knock against EVs. From 2020 through about 2023, some models carried **40–60% higher premiums** than comparable gas cars. As of 2025–2026, that gap has **narrowed dramatically**. Many mainstream EVs now sit within **5–15% of gas equivalents**, sometimes less, especially as more shops learn to repair them and parts pipelines normalize.

- Some states still offer **EV‑specific registration or tax incentives**, but the big federal purchase credits are gone for now.

- A few states charge **EV road‑use fees** to replace lost gas‑tax revenue. These can add a small annual cost, divide by 12 when comparing monthly.

- The new **federal auto‑loan interest deduction** (for qualifying U.S.-assembled vehicles) doesn’t discriminate between gas and EV; it can lower your after‑tax monthly cost on either, if you qualify.

Insurance tip for EV shoppers

How to lower your electric car monthly payment

If you’ve run the numbers and decided an EV is right for you, the next challenge is shaping that monthly payment into something that fits your life. You have more levers than just haggling over price.

Six ways to bring your EV’s real monthly cost down

1. Go used instead of new

Late‑model used EVs have seen some of the **sharpest price drops** in the market. You can often buy a 2‑ to 4‑year‑old EV for 30–45% less than its original MSRP, instant payment relief, plus lower depreciation.

2. Right‑size the battery

Bigger batteries cost more. If your life is mostly commuting and errands, you probably don’t need a 320‑mile battery. A **smaller‑pack EV** can shave thousands off the price and make your monthly payment feel civilized.

3. Optimize the loan, not just the price

A slightly higher sale price with a **better interest rate or shorter term** can cost you less over time than a rock‑bottom price and a punishing 84‑month loan. Run the full payment math before fixating on MSRP alone.

4. Charge smart at home

Ask your utility about **EV time‑of‑use rates** and schedule charging for off‑peak hours. Cutting 30–40% off your charging costs is like lowering your car payment without ever talking to a bank.

5. Avoid over‑optioning

Fancy wheels and panoramic roofs look great on Instagram and terrible on amortization schedules. Prioritize **range, safety tech, and battery health** over cosmetic upgrades if monthly cost is your north star.

6. Trade in or sell the right car

If you’re moving from two gas cars to **one EV plus one efficient gas car**, you may be able to sell the thirstier vehicle and free up cash for a bigger down payment, without sacrificing flexibility.

Why used EVs often beat gas cars on monthly cost

On the used market, the electric vs gas monthly payment battle is leaning heavily electric. Used EV prices corrected hard in 2024–2025 as new‑car supply improved and early lease returns hit the market. By late 2025, the **average used EV transaction price in the U.S. had slipped into the mid‑$20,000s**, undercutting many comparable gas models.

Why used EVs are a monthly‑budget sweet spot

Three structural advantages over used gas cars.

Front‑loaded depreciation

EVs tend to **lose value fastest in their first few years**, then level off. If you buy after that initial cliff, you’re paying for the car’s most stable years, not subsidizing someone else’s early‑adopter thrill ride.

Lower surprise‑repair risk

A used EV has fewer moving parts to fail expensively. Combine that with a **battery health report** and you can go into a purchase with more mechanical certainty than many used gas cars.

Ongoing fuel savings

Even if your payment is similar, **fuel and maintenance savings** give used EVs a huge edge on real monthly cost. Gas prices jump around; overnight kWh prices typically don’t.

Recharged is built around this reality. Our marketplace focuses on **used electric vehicles**, with battery‑health diagnostics, transparent pricing, and nationwide delivery. Every car gets a **Recharged Score Report** so when you’re comparing monthly cost, you’re not guessing about hidden problems.

FAQ: electric car vs gas car monthly payment

Frequently asked questions

Bottom line: electric vs gas monthly payment

If you only look at the **number on the finance manager’s screen**, electric cars often seem more expensive than gas cars in 2026. But a serious electric car vs gas car monthly payment comparison doesn’t stop at principal and interest. Once you add **fuel, maintenance, insurance, and tax effects**, many EVs, especially **used EVs**, turn out to be cheaper to live with month‑to‑month than their gas counterparts.

The practical way to shop is simple: pick a few candidates, get **real payment quotes** on each, then line up **estimated monthly fuel and maintenance** side by side. If the EV’s higher payment is more than offset by those savings, the decision makes itself. And if you want help finding a used electric car where the math actually works, Recharged can pair you with **battery‑verified used EVs**, straightforward financing, and expert guidance from your first search to the day it’s in your driveway.