If you’re asking yourself, “how much car payment for a used Tesla can I actually afford?”, you’re not alone. Between fast‑moving used prices and higher interest rates, it’s hard to know whether a Model 3 or Model Y will land closer to $350 a month… or $750. This guide walks through real‑world used Tesla price ranges, typical loan terms in 2026, and example payments so you can see what fits your budget before you start shopping.

Numbers in this guide

Why used Tesla payments are a moving target in 2026

Used Teslas don’t behave like a “normal” used car. After a steep decline in 2023–2025, average used Tesla pricing has recently ticked back up. In early 2026, typical used Model 3 prices hover in the mid‑$20,000s for 3–5‑year‑old cars, while Model Y crossovers sit around the high‑$20,000s to low‑$30,000s. At the same time, national used‑car loan rates have climbed into the high single digits, which means the monthly payment is driven as much by interest and term length as by the sticker price itself.

Used Tesla & financing snapshot, early 2026

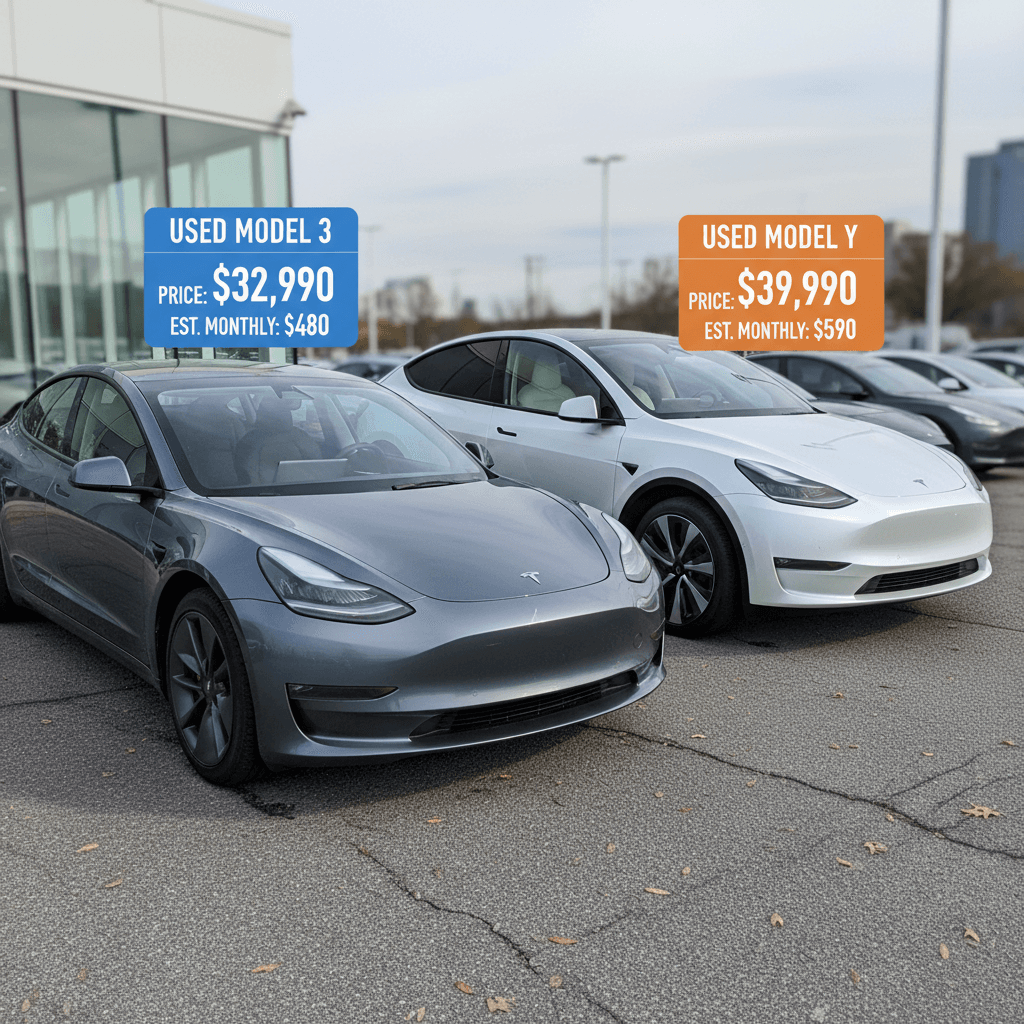

Typical used Tesla prices today

Exact pricing varies by mileage, trim, battery, and location, but here’s a realistic ballpark for used Teslas you’ll see in 2026. These are the kinds of cars many buyers are financing rather than paying cash for.

Typical used Tesla asking prices (2026 U.S. market)

Approximate price ranges for common used Tesla configurations that end up being financed. These are not Recharged list prices, just national ballparks.

| Model | Age & mileage example | Typical price range |

|---|---|---|

| Model 3 RWD/Long Range | 2018–2021 • 40k–70k mi | $18,000 – $26,000 |

| Model 3 RWD/Long Range | 2022–2023 • 15k–40k mi | $24,000 – $32,000 |

| Model Y Long Range | 2020–2022 • 40k–70k mi | $26,000 – $33,000 |

| Model Y Long Range/Performance | 2023–2024 • 15k–40k mi | $32,000 – $40,000 |

| Model S / Model X | 2017–2020 • 60k–100k+ mi | $28,000 – $50,000+ |

| Cybertruck & newer S/X | Very low supply | Highly variable, often premium‑priced |

Expect prices at the higher end of each range for low‑mileage, long‑range, or performance trims, and at the lower end for higher‑mileage or earlier builds.

Don’t shop by price alone

Quick answer: used Tesla payments by budget level

Let’s start with a high‑level view. Assuming a 9.5% APR, a 72‑month term, and no taxes or fees (we’ll add those later), here’s what different price points look like before down payment:

Rough monthly payments by used Tesla price

Assumes 9.5% APR, 72 months, zero down, excluding taxes/fees. Your rate and term may differ.

Budget shopper

$18,000 Tesla (older Model 3):

- Approx. $330–$340/mo before taxes/fees

- With $3,000 down: roughly $270/mo

Mainstream sweet spot

$25,000 Tesla (typical Model 3):

- Approx. $460–$470/mo before taxes/fees

- With $5,000 down: roughly $360/mo

Higher‑spec crossover

$32,000 Tesla (newer Model Y):

- Approx. $590–$610/mo before taxes/fees

- With $7,000 down: roughly $480/mo

30‑second affordability rule

How to estimate your used Tesla car payment

You don’t need a finance degree to get within $25–$50 of your likely payment. Use this simple three‑step framework any time you’re looking at a used Tesla listing.

3 steps to estimating your used Tesla payment

1. Nail down a realistic price range

Start with the listing price on a car you’d actually buy, not the cheapest Tesla you can find on the internet. For many shoppers that means a $22,000–$30,000 Model 3 or Model Y with reasonable mileage and clean history.

2. Choose a term and guess an APR

In early 2026, many used‑car borrowers land somewhere between <strong>8–11% APR</strong>, depending on credit and lender, with <strong>60–84‑month</strong> terms. If your credit is strong and you’re using a credit union or competitive online lender, you might plug in 7–8%; with fair credit or dealer‑arranged financing, 10–12% is safer to model.

3. Factor in down payment, taxes, and fees

Sales tax alone can add 5–10% depending on your state, and title/doc fees often add another few hundred dollars. If you’re putting $5,000 down on a $28,000 car, but taxes and fees add $2,000, your <strong>actual financed amount</strong> may still be close to $25,000.

The basic loan formula (without the math headache)

Auto lenders all use the same amortization math: your payment is based on principal (amount financed), interest rate, and term. For most buyers, the key levers are:

- Every extra $1,000 you borrow adds roughly $18–$22 per month on a 72‑month loan at today’s rates.

- Shortening from 72 to 60 months can raise your payment by 10–15%, but saves meaningful interest.

- A 2–3 point APR difference can swing payments by $30–$60 per month on a mid‑$20k Tesla.

Use tools, but sanity‑check the result

Online calculators are handy, but they assume clean credit and may ignore taxes or dealer fees. When you shop on Recharged, we surface transparent, lender‑backed payment estimates on each used EV, and our team can walk you through how different terms, down payments, and trade‑ins affect your monthly cost before you commit.

Sample loan scenarios for Model 3 and Model Y

Let’s run through some common used Tesla scenarios using realistic 2026 numbers. These examples assume average credit and market‑rate financing; if your credit is excellent or you’re using a high‑rate lender, adjust the APR up or down a couple of points.

Example used Tesla payments (estimates, not offers)

Illustrative payments for common used Tesla price points. All assume 9.5% APR. Taxes/fees will vary by state and dealer.

| Scenario | Vehicle & price | Term & APR | Down payment | Approx. payment |

|---|---|---|---|---|

| Value Model 3 | 2019 Model 3 RWD • $20,000 | 72 months @ 9.5% | $2,000 | ~$340/mo |

| Mainstream Model 3 | 2021 Model 3 Long Range • $25,000 | 72 months @ 9.5% | $3,000 | ~$410/mo |

| Newer Model 3 | 2023 Model 3 • $28,000 | 72 months @ 9.5% | $4,000 | ~$430–$450/mo |

| Practical Model Y | 2021 Model Y Long Range • $30,000 | 72 months @ 9.5% | $4,000 | ~$480–$500/mo |

| Newer Model Y | 2023 Model Y Long Range • $34,000 | 72 months @ 9.5% | $5,000 | ~$540–$560/mo |

| Performance or S/X | Higher‑spec Tesla • $40,000 | 72 months @ 9.5% | $5,000 | ~$650–$680/mo |

These are ballpark examples. A Recharged financing specialist can model precise scenarios, including local taxes and lender‑specific programs.

Beware of super‑long terms

Beyond the payment: other monthly Tesla costs

A smart budget looks beyond the car note. One reason many people can comfortably step up to a used Tesla is that fuel and maintenance are often lower than a comparable gas car, but insurance can be higher, and charging isn’t entirely free.

Key ongoing costs of owning a used Tesla

Think in terms of total monthly cost, not just the loan payment.

Charging vs. fuel

Electricity: Many Tesla owners pay the equivalent of $30–$70/month in home charging for typical commuting, depending on local rates and mileage. Supercharging on road trips adds extra cost but is still usually cheaper than gas.

Insurance

Insurance on a Tesla can run higher than a comparable gas sedan or crossover because of repair costs and advanced sensors. Get quotes for specific VINs before you finalize a purchase so the insurance bill doesn’t blow up your budget.

Maintenance & repairs

No oil changes and fewer moving parts are real advantages. But budget for tires, brakes, and out‑of‑warranty repairs, especially on older Model S or X. A healthy battery pack (verified by something like the Recharged Score) is critical to avoiding big surprises.

Connectivity & software

Teslas come with key software features baked in. Premium connectivity (for live traffic, streaming, etc.) is an optional monthly subscription. It’s not huge, but it’s another line item if you choose to keep it active.

Total cost can still beat gas

7 ways to lower your used Tesla payment

If the sample payments above feel a little rich, you have more levers than just “buy a cheaper car.” Here are practical ways to get a Tesla into a monthly range you’re comfortable with.

Strategies to shrink your monthly Tesla payment

1. Target the right model years

For Model 3 and Model Y, 3–6‑year‑old cars often hit the best payment sweet spot: new enough to have modern tech and range, old enough that first‑owner depreciation is behind you. Very new used cars can have near‑new prices without new‑car incentives.

2. Increase your down payment

Every extra $1,000 you put down can trim $18–$25 off a 72‑month payment at current rates. Use a tax refund, savings, or a trade‑in to reduce how much you finance.

3. Shop aggressively for APR

The interest rate is the most overlooked line on the contract. Get pre‑approved with a credit union or online lender before visiting a seller. A move from 11% to 8% on a $28,000 Tesla can shave <strong>$60+/month</strong> off your payment.

4. Consider a slightly shorter term

Yes, a 72‑ or 84‑month term looks affordable, but a 60‑month loan balances payment vs. equity much better. If the 60‑month payment is a stretch, aim for somewhere in between (66 or 72 months) and plan to pay extra when you can.

5. Be flexible on trim and options

Performance models, big wheels, and premium paints all come baked into the used price. Dropping from a Performance Model 3 to a Long Range, or from a 21‑inch wheel package to something more modest, can knock thousands off the financed amount.

6. Leverage your trade‑in strategically

A clean, in‑demand trade‑in can do more to lower your payment than a slightly lower Tesla price. At Recharged, you can get an <strong>instant offer or consignment option</strong> that often outperforms a traditional dealer trade.

7. Avoid costly add‑ons in the finance office

Extended warranties, paint protection, and other add‑ons can quietly add $30–$80/month. Some protections are worthwhile, but many can be bought later or from third parties for less. Decide what you truly need before you sit down to sign.

Focus on total out‑the‑door cost

Leasing vs financing a used Tesla

Most used Teslas in the U.S. are financed, not leased. Tesla itself doesn’t currently support traditional third‑party used leasing at scale, though some banks and credit unions do offer used‑EV lease products in select markets. Here’s how to think about the trade‑offs.

When leasing a used Tesla can make sense

- You want a lower monthly payment and are comfortable with mileage limits.

- You prefer to avoid long‑term battery or resale risk.

- A local credit union or specialty lender offers a competitive used‑EV lease.

Keep in mind: used leases can come with tighter mileage caps and wear‑and‑tear rules than new‑car leases. Read the fine print carefully.

When financing is the better play

- You plan to own the car for 5+ years and want to build equity.

- You drive more miles than a lease allows without penalties.

- You’ve found a competitively priced, well‑cared‑for Tesla with documented battery health (for example, via a Recharged Score Report).

With financing, you can sell or trade the Tesla on your own schedule, which matters in a fast‑evolving EV market.

How Recharged helps you right-size your payment

Figuring out “how much car payment for a used Tesla” you’re comfortable with is easier when the vehicle, battery, and financing details are all transparent. That’s exactly the problem Recharged was built to solve.

What Recharged brings to the table for used Tesla buyers

Transparent vehicles, real battery data, and flexible ways to buy or sell.

Verified battery health

Every EV on Recharged comes with a Recharged Score Report that includes third‑party battery diagnostics. You’re not guessing about range or degradation, critical inputs to long‑term cost of ownership.

Financing built for EVs

Recharged works with EV‑friendly lenders to offer competitive used‑EV financing. You can see estimated payments online, apply digitally, and understand how different terms and down payments change your monthly cost.

Modern, flexible buying experience

Shop and finance entirely online, opt for nationwide delivery, or visit our Experience Center in Richmond, VA. Have a vehicle to sell? Use our instant‑offer or consignment options to maximize trade‑in value and shrink your Tesla payment.

Start with your monthly comfort zone

FAQ: used Tesla payments and affordability

Frequently asked questions about used Tesla payments

A used Tesla can absolutely fit into a reasonable monthly budget, but only if you treat the payment as one piece of a bigger affordability picture. Start with an honest look at your take‑home pay, set a target payment range, and then work backward through price, APR, term, and down payment until the math supports the Tesla you want. With transparent battery health data, fair‑market pricing, and EV‑savvy financing partners, Recharged is built to make that process straightforward so you can enjoy the benefits of electric driving without losing sleep over the bill.